On Friday, March 10, 2023, Silicon Valley Bank was shut down by bank regulators. This piece is meant to be an overview of events. Note this is an event where next steps are being updated daily, so answers are subject to change.

Information available as of March 13, 2023:

What happened? Silicon Valley Bank (SVB) collapsed last week, with the FDIC now in control of the bank. The collapse of SVB marks the 2nd largest bank failure in US history (Washington Mutual was first), and the first large bank failure since the Great Financial Crisis (2008).

Why did SVB collapse? There are several challenges that SVB was facing. For one, the bank’s clients were heavily concentrated in the tech industry, with its deposits booming along with the tech industry. However, as the tech industry has suffered as of late, the money that was previously deposited was now being withdrawn in large amounts, at the same time the bank suffered large losses in their bond portfolio due to rising interest rates. In other words, there was a large mismatch between their deposits (liabilities) and assets. The bank needed fresh capital in order to meet withdrawal demand but wasn’t able to find it quick enough.

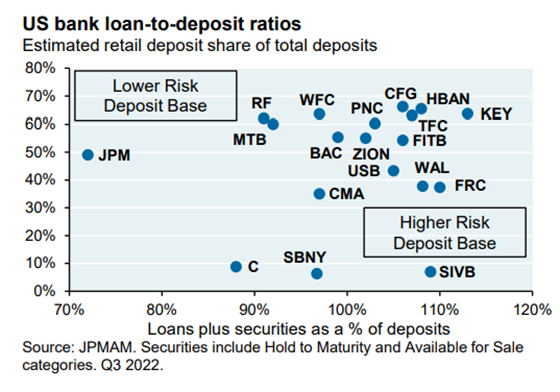

Are more banks going to fail? According to JP Morgan Asset Management (see chart)), SVB “was in a league of its own” with both a very high level of loans plus securities as deposits and a very low amount of retail deposits as a percentage of total deposits (retail deposits are generally stickier).

While it is always possible that more banks may fail, it is currently not expected that the issues facing SVB are systemic, or that the banking industry as a whole is under immediate pressure. In fact, the measures that the Fed ia taking right now, including the creation of the new Bank Term Funding Program, are meant to provide support and confidence for the banking system as a whole.

Will SVB clients be made whole for the deposits? For clients whose deposits were within FDIC guidelines, those clients will be made whole. For those clients whose deposits exceeded FDIC limits, an announcement was made on March 12 that all depositors will be made whole, even if their deposits exceeded FDIC limits. The decision was made to do this in order to provide confidence to the entire banking system and prevent runs on other banks. However, according to the statement, bondholders of SVB wouldn’t be protected, so the move by regulators is not technically considered a bailout.

Are the recent failures of Signature Bank and Silvergate Bank related to the failure of Silicon Valley Bank? Like SVB, both Signature Bank and Silvergate bank were considered somewhat alternative banks as they were considered two of the most crypto-friendly banks (per the Wall Street Journal, 27% of assets in Signature Bank in 2022 were from digital-asset clients). The recent struggles in crypto (e.g. the recent collapse of FTX, the crypto exchange from Sam Bankman-Fried) left both banks vulnerable to the runs on deposits that occurred.

Should I be concerned about my bank failing? As we previously described, the failure of SVB is not expected to cause systemic bank failures. At the same time, investors should expect to see volatility in bank stock prices as some uncertainty remains.

Is there anything I should do with my bank deposits today? The failure of SVB is a great reminder to make sure that your bank deposits meet FDIC guidelines. This FDIC website includes a great chart showing coverage limits by account ownership.Should I make adjustments to my investment portfolio? We know that markets don’t like uncertainty, so we are not surprised to see volatility across bond and stock markets in the short term. At the same time, we don’t suggest knee-jerk reactions to your investment portfolio. Our portfolios are diversified and allocated with your level of risk tolerance in mind. Therefore, the theme of staying the course is still prudent at this time.